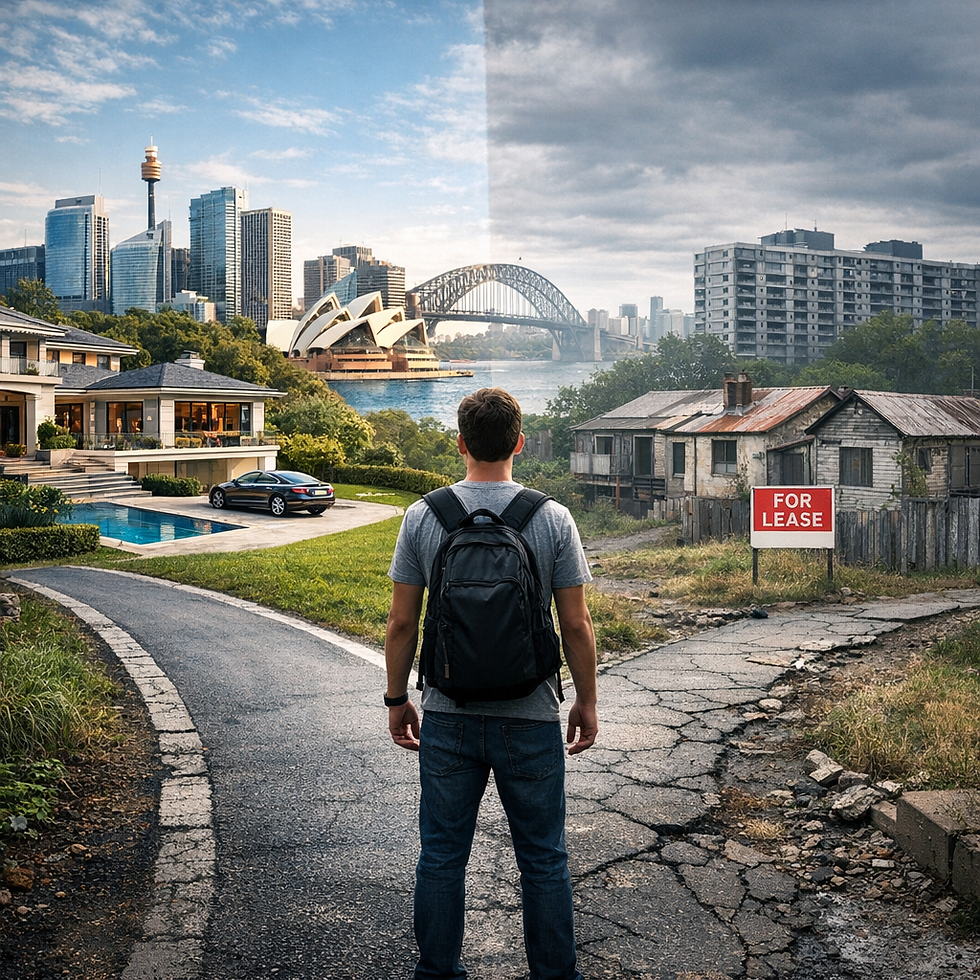

The Great Australian Divide

- Bain Dohne

- Mar 2

- 3 min read

Housing, Incentives and the Leadership Question We’re Avoiding

The AFR headline was blunt:

“No affordable houses for first home buyers.”

That is not a cultural complaint. It is a structural signal.

For most of Australia’s post-war history, housing functioned as a stabiliser. A median income could plausibly buy a median home. Ownership was not effortless — but it was attainable without inheritance.

That alignment has shifted.

Over the past two decades, dwelling values have grown faster than wages in a sustained way. Not just during booms. Across cycles. The gap has compounded.

And compounding changes societies.

When Shelter Becomes Strategy

Housing is no longer just a home.

For many Australians, it is:

The primary retirement strategy

The family balance sheet

A hedge against inflation

A wealth transfer vehicle

That transformation didn’t happen accidentally.

It evolved through policy design.

Negative gearing allows investors to deduct rental losses against other income. On its own, that mechanism exists in other countries. But Australia pairs it with a 50% capital gains tax discount.

That combination matters.

It makes leveraged property investment particularly attractive over time.

Was that the intention?

Probably not in the way it’s played out.

But policy outcomes don’t care about original intent.

They care about incentives.

And incentives shape behaviour.

The COVID Acceleration

Then came the pandemic.

Ultra-low interest rates.Fiscal stimulus.Shift in lifestyle preferences. Supply constraints.

Prices surged — not only in Australia, but globally.

However, Australia entered that period already stretched relative to incomes. So when the surge came, it lifted an already elevated base.

When rates rose, prices softened in some areas — but the affordability reset never truly arrived.

The ladder moved higher.

And for many younger Australians, further away.

The Intergenerational Question

Here is the tension.

If prices fall sharply, existing owners lose wealth.

If prices continue rising faster than wages, non-owners lose opportunity.

Both outcomes have consequences.

This is not a simple generational conflict. Many younger Australians benefit from family support. Many older Australians support reform.

But the structure matters.

When entry increasingly depends on intergenerational transfer rather than income, wealth becomes inherited rather than earned.

That shifts social mobility.

And mobility is oxygen for a democracy.

What Have Other Countries Tried?

This isn’t theoretical.

The UK reduced landlord tax concessions. Investor returns compressed — but rental markets tightened.

New Zealand removed interest deductibility for many investors. Investor activity slowed — but rents rose in parts of the market.

Singapore intervenes heavily, combining ownership restrictions with large-scale public housing. It works — but within a highly centralised governance model.

There is no painless fix.

There is no silver bullet.

Every lever redistributes cost.

The real question is whether the cost is managed early or forced later.

So What Is the Leadership Question?

Housing is not just an economic debate.

It is a leadership test.

Are we willing to:

Adjust tax settings gradually to realign incentives?

Reform planning systems despite local resistance?

Accept slower asset growth in exchange for broader opportunity?

Have an honest conversation about intergenerational equity?

Or do we protect the status quo because it is politically safer?

Australia has historically chosen pragmatic reform over rupture. Compulsory voting. Wage arbitration. Superannuation. Medicare.

Each was controversial at inception.

Each required long-term thinking over short-term applause.

The housing question demands the same maturity.

Let’s Provoke the Debate

Here are uncomfortable realities worth discussing:

Housing has become a low-risk, tax-advantaged asset class.

Australia has one of the highest household debt-to-income ratios in the developed world.

Younger Australians are entering the market later — or not at all.

Policy settings created in one economic era are operating in a very different one.

The divide is not inevitable.

But it will not close itself.

A Question for Both Generations

If meaningful housing reform occurs, who should bear the primary cost?

Investors?

Existing homeowners?

Taxpayers collectively?

Or should we allow market forces to determine the outcome?

There is no morally clean answer.

But avoiding the question is itself a decision.

And leadership is not avoiding hard questions.

It is confronting them before they become crises.

For the LinkedIn series, follow the links below:

Comments